By Sudhanshu Kanwar, CFA, FRM, CQF

“Hedging Delta protects you against yesterday’s risk, Hedging Vomma and Ultima prepares you for tomorrow’s crash”

Abstract

Historical economic landscape shocks from Black Monday to the COVID-19 crisis have repeatedly exposed shortcomings of traditional Delta-centric hedging. Successful risk management demands understanding of higher-order Greeks—particularly Vomma, Zomma, and Ultima—that reveal how options behave under extreme volatility conditions. Through detailed real-world case studies, technical explanations of Greeks across moneyness (ITM, ATM, OTM), and role-specific applications, this article illustrates how incorporating these sensitivities can significantly enhance portfolio resilience and profitability during crises.

1. Introduction

In derivatives pricing, standard practice emphasizes first-order Greeks such as Delta and Vega. While these metrics effectively manage linear sensitivities under normal economic conditions, economic crises repeatedly demonstrate their inadequacy during volatility spikes and tail events. The real differentiation occurs with higher-order Greeks (Gamma, Vomma, Zomma, Ultima), which describe non-linear sensitivities and interactions essential for precise risk modeling and effective hedging in turbulent economic landscapes.

2. Real-World Use Cases: Advanced Greeks in Action

2.1 The 2008 Korean Knock-In Option Disaster: Zomma and Vera Ignored

During 2007-2008, numerous South Korean exporters sold exotic FX knock-in options on KRW/USD. These options initially appeared harmless, being Delta- and Vega-hedged under stable volatility assumptions. However, the 2008 economic crisis triggered an unprecedented spike in both volatility and interest rates simultaneously. Traders had overlooked Zomma (Gamma sensitivity to volatility) and Vera (Rho sensitivity to volatility), failing to recognize how dramatically Gamma and interest rate exposures could shift under such conditions. As volatility surged, the knock-in barriers were breached unexpectedly, converting previously low-risk positions into deep, loss-making instruments. The resultant unhedged Zomma and Vera exposures translated into more than $2 billion in corporate losses, devastating firms that relied solely on first-order hedging.

2.2 Universa Tail Hedge Fund in 2020: Ultima and Vomma Mastery

Amidst the COVID-19 pandemic, Universa Allocations, a tail-risk fund advised by Nassim Taleb and run by Mark Spitznagel, had strategically purchased deep out-of-the-money put options characterized by significant exposure to Ultima (the convexity of Vomma) and Vomma (Vega’s sensitivity to volatility). These instruments had very low initial premiums and seemingly negligible immediate payoff profiles under normal economic conditions. However, when economic landscapes collapsed, volatility-of-volatility surged dramatically. This explosive increase triggered enormous payoffs, with the fund achieving returns exceeding 4,000% on just 1% of capital deployed. Universa’s extraordinary returns resulted not merely from predicting increased volatility but specifically from structuring positions that profited exponentially as volatility itself accelerated, illustrating the power of properly hedging third-order sensitivities like Ultima.

2.3 Flash Crash 2010: Gamma Neutral ≠ Risk Neutral

On May 6, 2010, a rapid intraday economic decline—later dubbed the “Flash Crash”—caused severe disruption for many exchanging desks operating under Gamma-neutral strategies. Although traders hedged Gamma, they overlooked second-order effects such as Speed (the rate of Gamma change with underlying price) and Charm (the rate at which Delta decays with time). During rapid economic movements, these overlooked Greeks became dominant, causing instantaneous and unanticipated shifts in Delta exposure. Traders were left attempting frantic hedges as their models, built around static Gamma assumptions, failed to capture real-time exposure shifts. This scenario underscores the vital need for continuously accounting for these subtle but impactful sensitivities, particularly in automated, high-frequency exchanging environments.

2.4 2022 Fed Tightening Cycle: The Vega Trap and Vomma Blindspot

Throughout 2022, following aggressive Federal Reserve interest rate hikes, volatility in the economic landscape behaved atypically. Many traders shorted Vega, predicting implied volatility would decline post-policy adjustments. However, persistent geopolitical tensions (notably the Russia-Ukraine war) and sustained inflation fears kept volatility elevated longer than anticipated. Crucially, traders ignored their exposure to Vomma (convexity of Vega)—the sensitivity of their volatility positions to volatility-of-volatility itself. Without appropriate Vomma hedging, these short-volatility positions incurred prolonged losses as Vega failed to normalize swiftly. This subtle but significant oversight illustrates the hidden dangers of relying solely on first-order volatility exposure metrics.

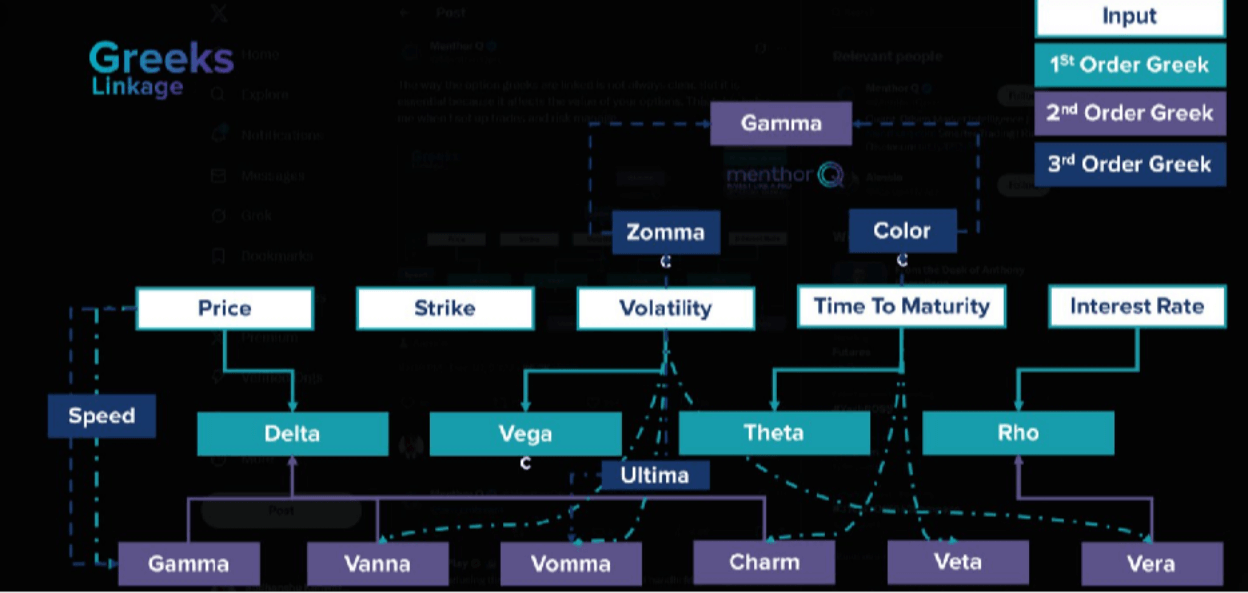

3. Technical Insights: Greeks Across Option Moneyness

3.1 First-Order Greeks

| Greek | ITM | ATM | OTM | Implications |

| Delta | ~1 (Calls)/-1 (Puts) | 0.5 | ~0 | Directional exposure highest ITM. |

| Vega | Moderate | Maximum | Moderate | ATM options most sensitive to vol. |

| Theta | Moderate negative | Most negative | Slight negative | ATM loses value quickest near expiry. |

| Rho | Highest (long-dated) | Moderate | Minimal | Significant mainly for long-duration ITM options. |

3.1 First-Order Greeks

| Greek | ITM | ATM | OTM | Implications |

| Gamma | Low | Maximum | Low | ATM highest near expiry—critical for scalping. |

| Vomma | Moderate | Maximum | Moderate | ATM Vomma high—significant risk during volatility shocks. |

| Vanna | Moderate | High | Moderate | Important for skew-sensitive hedging. |

| Charm | Moderate | High near expiry | Low | Critical to Delta decay management. |

3.3 Third-Order Greeks

| Greek | ITM | ATM | OTM | Implications |

| Zomma | Low | Moderate | Moderate | Important in barrier options and volatility regime shifts. |

| Speed | Minimal | Moderate-High | Minimal | Crucial around binary events (e.g., earnings). |

| Color | Minimal | Moderate | Minimal | Weekend and holiday risk modeling. |

| Ultima | Low | Moderate-High | Very high | Tail hedging via deep OTM puts. |

| Veta | Minimal | Moderate | Minimal | Important for long-dated volatility sellers. |

| Vera | Low | Moderate (FX/IR) | Minimal | Crucial during dual volatility-rate shocks. |

4. Practical Thresholds for Monitoring Greeks

- Gamma: Monitor closely when approaching expiry, especially if Gamma exceeds 0.3 (Delta shifts rapidly).

- Vega: Pay close attention if Vega surpasses 0.2, particularly during uncertain macro periods.

- Vomma: Crucial if Vega >0.2; indicates positions sensitive to volatility-of-volatility spikes.

- Ultima: Key metric in tail-risk positioning; look for exponential payoff potential.

5. Greek Relevance by Role

- Quantitative Analysts: Incorporate Gamma, Vomma, Zomma, Ultima into advanced volatility surfaces and scenario analyses.

- Traders: Actively manage Gamma, Vega, Charm to maintain effective hedges intraday and during volatile periods.

- Portfolio Managers: Track Theta, Vega, Veta, and Rho for optimizing carry, macro-risk overlay strategies, and asset allocation.

- Risk Managers: Prioritize Vomma, Ultima, Color, Vera for comprehensive stress testing and nonlinear risk forecasting.

6. Conclusion

Economic crises consistently demonstrate that reliance on first-order Greeks is insufficient. Higher-order sensitivities—especially Vomma, Zomma, and Ultima—offer necessary tools for managing severe economic volatility. The dramatic success of Universa’s tail-hedging strategy and the devastating failure in the Korean knock-in disaster illustrate how crucial these overlooked metrics are for robust, resilient economic risk management.